Battery companies suffer from two extrusions positive and negative prices are still strong

In the pressure on the main engine plant, the automobile cuts the price, forcing the industry chain to share the cost of each link, the battery company suffers two squeezes, and the profitability declines. The raw materials such as lithium, cobalt, and nickel have increased, and the upstream manufacturers are stealing. fun".

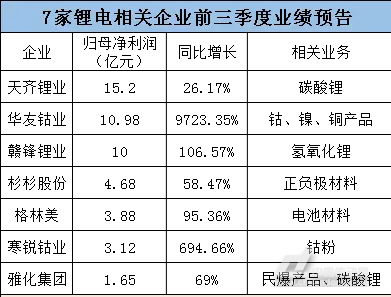

7 companies' net profit for the first three quarters exceeds 100 million yuan

The reporter carried out statistics on the forecast results of the seven lithium battery upstream manufacturers in the first three quarters. From the overall situation, the net profits of the seven companies have all experienced different degrees of growth. Among them, the highest is Tian Qi Lithium 1.52 billion yuan, and the lowest is Yihua Group 165 million yuan.

Judging from the net profit stratification situation, Tianqi Lithium, Huayou Cobalt, and Yanfeng Lithium have a profit of over RMB 1 billion, and the three net profit margins of Shanshan, Glimme and Hanrui are relatively small.

From the perspective of the year-on-year growth in net profit, there is a wide gap. Huayou Cobalt Industry led the industry with 9723.35%; Hanrui Cobalt Industry and Yufeng Lithium ranked second and third respectively.

Positive and negative prices are still strong

Positive market

In the first three quarters of 2017, it was the cathode material supplier that had earned a lot of pounds. The seven companies mentioned above were cathode material suppliers (in which Shanshan shares both positive and negative electrodes). Due to the increase in the sales volume of new energy vehicles, due to the double-pointing policy, Tianchai added fire. As cobalt and lithium, which are the basic raw materials for cathode materials, prices have risen sharply in different periods due to the imbalance between supply and demand, and they have remained at high levels.

It is worth mentioning that the ternary cathode is gradually surpassing the cathode of lithium iron to expand its market share.

1 In terms of supply and demand, in the third quarter of 2017, the domestic triple positive capacity reached 90,000 tons, the output was 24,500 tons and the chain growth was 15%; while the production of lithium iron decreased by 7%.

2 In terms of price, the price of lithium cobalt increased in the third quarter of the upper reaches, and some of the precursor manufacturers were forced to suspend production due to environmental inspections. The prices of cathode materials for Sanyuan and Lithium were all increased, and the price of Sanyuan Materials in the third quarter was 20. The third quarter price of yuan/ton and iron-lithium materials was 95,000 yuan/ton.

3 The triple positive market is still fragmented. Long-Term Lithium ranks first with 11% market share and CR3 with 31%. The Lithium-Ion cathode market is ranked first with 18% market share and CR3 49%.

Negative market

The price increase of anode materials, due to the sudden increase in the demand for graphite electrodes, stimulated the price of needle coke in negative electrode materials to rise sharply. At the same time, under the influence of factors such as environmental inspections and limited graphitization capacity, negative electrode material prices rebounded in the third quarter.

1 In terms of supply, in the third quarter of 2017, the domestic negative capacity of artificial graphite reached 63,000 tons, and the output was 32,400 tons; the output of natural graphite anode reached 24,000 tons, and the output was 10,900 tons.

Comparing the two negative electrode materials, it can be seen that the output of artificial graphite in the third quarter increased by 19%, while the natural graphite output increased by 7% from the previous month, and the penetration rate of artificial graphite further increased.

2 In terms of price, the price of artificial graphite in the third quarter was 55,000 yuan/ton (up 30% from the previous month), and the price of natural graphite in the third quarter was 35,000 yuan/ton (up 9% from the previous quarter).

3 negative market is more concentrated. The world's first cathode material, anode material for the country's second Shanshangufen, its artificial graphite ranked first in market share of 31%; and natural graphite, BTR still more than 57% market share ranked first.

In general, under the dual effects of tight upstream supply and sudden increase in downstream demand, raw material prices for power batteries have continued to maintain a sustained upward trend, which has led to a substantial increase in the profitability of material companies. With the increase in sales of new energy vehicles and the escaping of ternary power batteries, it is expected that the prices of cobalt and lithium materials will continue to rise.

In addition, from January to August 2017, sales of new energy vehicles were 320,000, an increase of 30.2% year-on-year, and the annual sales target was 700,000. The distance of the target of 700,000 and nearly 400,000, so the next time, at the same time fight the sales, battery production capacity increase, it will be extended to areas downstream materials, materials to further enhance their market competitiveness and product profitability .

Giant Led Screen,Round Led Screen,Advertising Led Display Screen,Led Screen Indoor

Shenzhen Apexls Optoelectronic Co., Ltd , http://www.apexls-display.com